1

2

3

4

5

6

7

8

9

10

11

When the PC was invented, I saw the future in front of me. Opportunity knocked and I answered. I did every job you could do on them.

The head of our DP department said we would have no need for any PC’s. It was as clear to me then as the PC you have for your everyday use (or more than 1) that this was going to be the future. I got in very early to the phenomenon and a decision that early in a career was very fortunate.

I retired early because of that decision and where it took me.

Cars

Chevy Now Makes New 350, 400, and 409 V8s — Just Like the Old Days

Ferrari Reportedly Tells Buyers To Buy Unpopular Luce To Move Up On Wait List

Artificial Intelligence

20 College Majors Most Exposed yo AI Job Disruption

Religion

Gallup Poll: Women, Youth Led American Departure from Religion Over Past Decade – Social media, peer pressure and feminism, my 2 cents

Golf

The 20 U.S. Open Courses That Have Produced The Most Holes-In-One

Climate Hoax

Travel

Airline announces world’s longest nonstop flight that will carry passengers 22 hours – that’s way too long to be in a tube with a few hundred others who didn’t shower either. I’d never take this flight

Harvard

Students at Harvard Twice as Likely as General Population to Experience Mental Illness – I knew this decades ago. I had to work with the graduates and to a person they were useless.

Trash Talking

The 9 Most Vicious Trash-Talkers In The History Of The NBA

Obama Library and Borg Cube

Bill Maher: Obama’s $850M Library Looks Like “Aliens Built It in Dubai” — Calls Audience “Liars”

Females working for Satan since the beginning of time

Feminists Are Increasingly Joining “Witchcraft Communes” To Fill The Spiritual Void – Aren’t they bad enough already?

(Note: this is an update. Will B. Done pointed out that the links didn’t work, so I fixed them so you can click and enjoy)

I’ve written this blog since August of 2005. It was originally meant for my job in analyst relations, but took a turn when I retired in 2011. It’s morphed into any number of things from humor, sarcasm, anti-Covid Jab and my ramblings on life.

I start Chemotherapy next week, so it’s going to slow down considerably, although I’ll post from time to time. I’ve scheduled some posts so it will look like I’m continuing as I suffer through the poison they will be putting in me. You’ll read something every day this week, but I’m not collecting headlines. I hope to be back, I just know I won’t have any energy

I want to say that I’ve enjoyed the 10’s of thousands of comments, and different groups of readers.

I mostly wrote it as it is my favorite form of communication. If you read anything about me, you know I’m introverted so small talk isn’t my greatest strength.

I pulled the list of top posts. It’s funny to me that my most successful post is Euphemisms for Stupid, which was number one on Google for over 10 years in that category.

As I look at the list, I see various stages of my life and different careers. I see family, pets and co-workers. I’m especially proud of My Dad. It’s the post, On Behalf of the President of the United States.

I wish you all the best and a longer life than me.

It’s not over, but for sure will not be as consistent.

If anyone wants to guest post, send it to me simonize@protonmail.com and I’ll try to put it up and give you credit.

Posts & pages

Views

Work

Welfare Enrollment Drops Sharply Following New Federal Work Requirements – having to get a job makes things different.

Head Injury

Nottingham Forrest’s Morgan Gibbs-White Suffered One Of The Most Gruesome Facial Injuries You’ll Ever See; Skull Exposed Through The Wound – strange to see someone’s skull while they are alive

Travel

Cars

426/425 HP Hemi V-8, 1 of 59 Produced, Broadcast Sheet

Jerry Seinfeld rips electric cars as ‘stupid virtue signal,’ has zero interest – EVs are ‘all BS’ and questioned how environmentally friendly they actually are – from the man with one of the best Porsche collections in the world

Ferrari Skids As Wartime Disruptions Hit Deliveries

Ford Sales Post Sharp 14.4% Decline In April As EV & Hybrid Sales Plunge

Women’s sports

University Of Washington Women’s Soccer Team Loses Preseason Scrimmage To A Group Of 14-Year-Old Boys – why I call BS on equal pay. They don’t play as well and it should be meritocracy. Just watch Mens and womens Tennis for example. Res ipsa loquitur

I could say getting married, but that worked out.

I suppose it is packing up from Florida, where I’d lived my whole life, and moving the entire family to North Carolina without ever having been there. It was a new job, a new house, a new career, and a complete change of life. I was in my late 30’s so it was not one of those teenage roadtrips.

As it turned out, it set me on the course of a great place to live, out of the Florida heat and tourist trap living, and gave me financial security for the rest of my life.

While the job was still in the Tech industry, it was in an area that I’d never been a part of. In the interview, I got asked what I knew about Networking Hardware, and I (honestly) said that I was not well-versed.

My answer was that since this was a job dealing with the press, I knew what they wanted and my strengths were there. I nailed the interview, and we just up and left in a couple of weeks.

I was working in the finance division of Burdines Department Stores when the IBM-PC was announced. I had been working with a System 34 and immediately saw my future. This was around 1981.

Here is what I was doing at the time.

The head of our DP department said there would be no need for PC’s because you couldn’t do anything with them. So I left

Within months, I was working for the largest Independent PC store in the country and balls-deep into the world of PCs.

It was the biggest open door to opportunity that I’ve seen in my whole life. I knew there was a huge future, and I was about to get in on the ground floor at the very beginning. I started with CPM on Apple II and DOS 1.0 on the PC.

They weren’t ubiquitous back then. I learned more by fixing them and figuring out why they crashed than almost everyone I knew.

The other decision I view as one of my best is to not take the COVID-19 jab. While everyone pressured me to get it, I held my ground. To this day, I don’t regret it and never have to worry about what they put into it. You can never get un-jabbed.

How The Left Are Elitists

The Left Is Baffled — but Still Repulsed — by the White Working Class – That’s what happens when you think you are better than others. Goes right along with Bitter clingers to guns, bible and God and a basket of deplorables. They hate the majority of Americans

Victor Davis Hanson Breaks Down a Huge Problem for the Democrats: ‘They Despise the Working Class’

Best and Worst States to work from home

the best and worst states to work from home.

Elevator

How the elevator revolutionized how we live.

Obama Borg Cube Library

Obama’s Presidential Library Exposed for Discriminating Against Illegal Aliens…

Cars

Iran

ART OF THE DEAL: Pressure, escalation, chaos… then leverage a deal, and now the results

Illegals

‘I just don’t wanna die’: 15-year-old American begs for his life before illegal murders him… This is for all the people who think the illegals should be allowed in and allowed to stay. This is who they are. If you want them to be in, may they visit you.

Nutrients For Your Eyes

Five Nutrients That Improve Your Eyesight in a Screen Dominated World

Baseball Fights

No Pupils

Top Cities For Young Pro’s

ranking the top US cities for young professionals.

How Biden Screwed America Over With Illegals Exposed (see Rape below)

Tom Homan Just Revealed the Dark Secret Inside Biden’s Immigration Scam

Another Politician Caught In the Covid Money Scam

ANOTHER Democrat in Hot Water Over Covid-Linked Fraud

BLM Activist Ordered To Pay Back $224,000 In COVID Relief Funds, Donations

Racism Is Racism, Even When The Victims Are White

10 of the World’s oldest Dog Breeds

Who Created Covid At UNC-CH?

Did Ralph Baric at UNC Create SARS-CoV-2? – If he didn’t, he sure as hell had something to do with it because they also created the Moderna version of the jab. I lived near their, it other than basketball, there was a lof of shit associated with that school (and Duke)

At Least It’s Not Soylent Green

‘Disturbing to say the least’: State advances bill to turn dead humans into actual fertilizer

Glad They Got Their Priorities Right

Two Years Later, No Key Bridge As Maryland Dems Focus On Tampons In Men’s Bathrooms – what a bunch of douche canoes

When you are so woke, you are stupid as shit

Pa. House Dems Pull Women’s Month Resolution to Escape Having to Define ‘Woman’ – We’ve not had a problem knowing what a woman was for thousands of years, until woke ruined everything. Let me clear it up. If you were born with a dick, you ain’t one, ever.

Rape, A clear reason not to bring in Immigrants.

African migrant is asked about rape, and his response leaves the journalist gobsmacked… He’s not even botherd by it. Don’t let these MF’s in and kick people like this out.

Social Media

“Don’t Be Evil”: Google’s Motto Becomes A Jury Verdict In California – They’ve been evil for the last 2 decades

Traitor

Winter Olympian Who Cried About ICE Goes Home Empty-Handed — Whines That Trump Criticism Made It ‘Hardest Two Weeks of My Life’ – forking pussy, grow a set and quit whining.

Work

These Are The Most Dangerous Fields Of Work – notice that they are all done by men?

Invasion

The Muslim Conquest of Europe Is Nearly Complete With Population at 50 Million and Growing [VIDEO]

Sore Loser

Munich Meltdown: Clintons Rant and Rave Against Trump in Europe – she can’t get over losing, Trump released Epstein records and they didn’t get their one world Governement. Oh, and they are assholes

Obama

Bombshell Investigation Exposes Cover-up of Obama Center Taxpayer Scam – screws taxpayers out of money to build his Library

Health

Ranked: The World’s 10 Deadliest Viruses by Fatality Rate

Cars

Fans Will Have a Tough Time Ordering the Facelifted 2027 Nissan Z

McDonald’s

Mapped: The Countries With the Most McDonald’s Per Person

Do you trust your instincts?

Always.

I somehow was blessed with an innate ability for pattern recognition. I can see disparate things happening, put them together, and know what a good opportunity is. I didn’t know it until things fell into place for me, and I thought everyone saw what I did, but I was wrong.

Here are a couple of examples. I’ll be as matter-of-fact as I can.

I chose a career in personal computers when I didn’t know what to do. They couldn’t do anything, except for VisiCalc, but I saw it as my future before they introduced the IBM PC. The head of a major company said he saw a demand for about 5 of them, and why would you want one on your desk. I made a career out of it. People thought I was chasing my tail at the time.

I had things in life I wanted to do, and knew that if I wanted to retire by 55, I’d have to start before 30. I finally left at 53, and people at IBM were still living paycheck to paycheck up in NY. I refused two job offers to move there to live where the cost of living was 30% less. Money is made 2 ways: make more and spend less. I did both. Plus, I didn’t have to live in NY.

It was clear to me that COVID was a hoax from the beginning, and I refused the jab when the sheep were lining up for it. Once I saw that the Government was forcing an untried and untested treatment they called a vaccine, I knew not to take it. I had studied gene editing and knew it was untested and untrustworthy. My whole family and all my friends thought I was nuts. They couldn’t wait to get it and thought I was risking my life by not getting it. They all got Covid anyway.

My Son in Law, who has patents and is a chip designer said I was smart, so why didn’t I get it? I’m not a lemming, that’s why. It was clear to me that Ivermectin and Hydroxychloroquine were the cure. They tried so hard to ban (and got the media to promote that it was bad) it that I knew to research it and found it to be the cure. I never regretted not getting jabbed, and the rest of the family now wishes they had made my decision. They rushed to get it because they were told that it was “safe and effective”. I called BS. We don’t talk about it because they hate me being right on that one. Thanksgiving is next week, and it will come up like Trump.

I never doubted that Trump would beat Hillary when Scott Adams talked about his ability to use persuasion techniques. I was an island on that one also. I was less certain in 2020, as the evidence of rigging and judicial interference was too overwhelming. Anybody could have called the 2024 election, so I don’t take any credit.

I worked in sustainability for IBM around 2009, but I knew Climate change was a scam when they worried about the hole in the Ozone layer in the late 1990’s. I knew it was a lie from the start, and we found out this week from none other than Bill Gates that it isn’t true, but rather a power grab. I read yesterday that the Ozone hole was mysteriously closing. Again, I was on an island calling BS.

I also have spatial Awareness that I got from my father. I can see how things fit together. It’s as clear as day when others are just arranging objects. Between that and pattern recognition, some things are clear to me as to their truth or the path I should take.

So yes, I trust my instincts.

The cesspool that is TikTok is overflowing with mentally broken TDS sufferers ‘creating’ endless content consisting of every ‘Orange man bad’ thought that fizzles to the surface of their dwindling brain matter.

One cannot go swimming in there for long before it starts to eat away at one’s soul, but this nugget is particularly funny.

This… person asked for advice on what “MAGA men” find attractive so she can do the opposite.

You can smell red flags from this side of the country. We are tired of that girl liberal shit that ruins everything and makes them so unhappy.

The minute you make a guy meet your cats and take you to a vegan restaurant, it’s over.

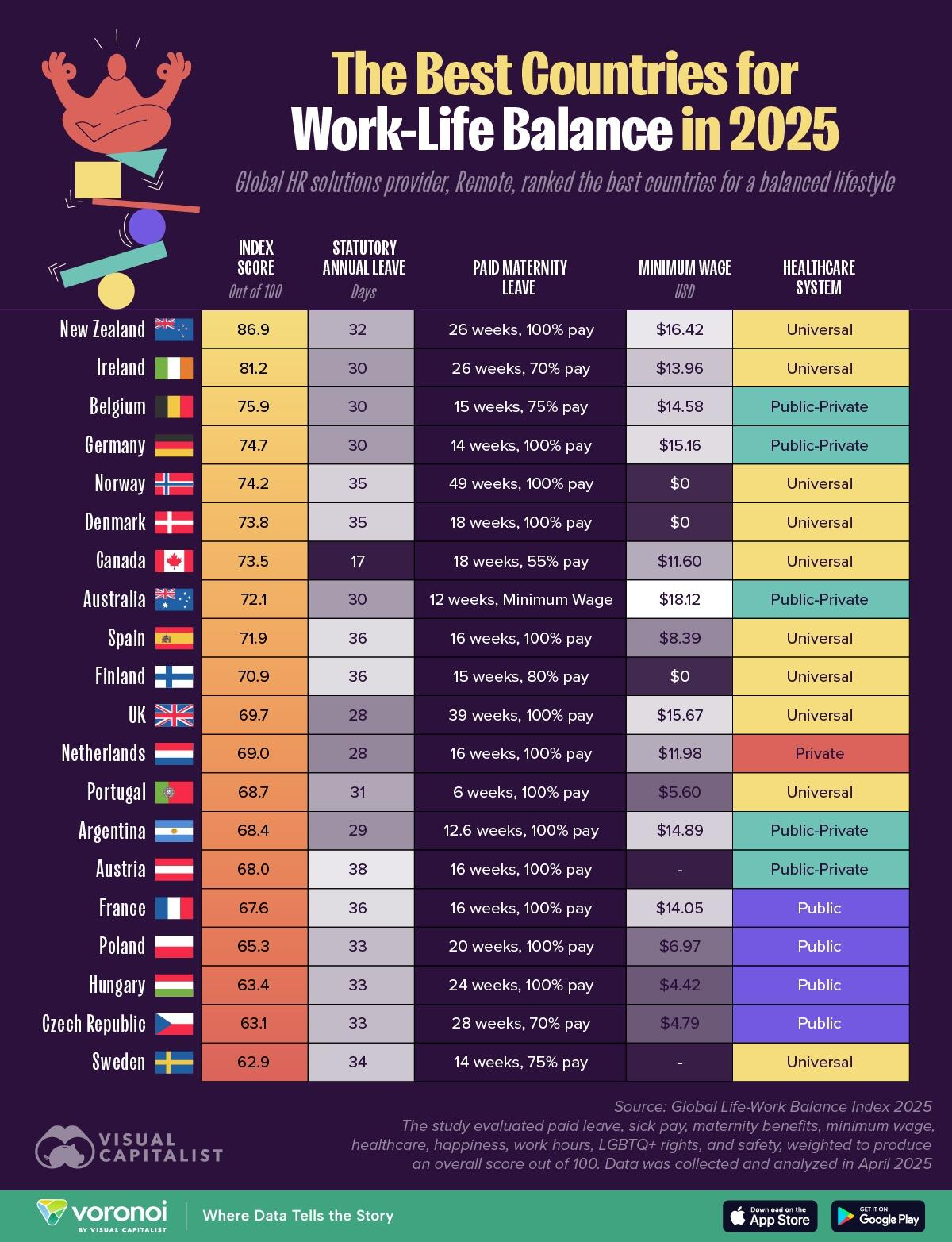

It’s bullshit. The top countries and a socialist system that gives them free (taxed at over 50% from the other citizens.

Nothing is free, starting with work/life balance. All this means is that they fuck off a lot in some countries.

object lesson number 4,271 in:

while you may control the lesson plan, the teaching, and even the access, you cannot control that which is learned.

the lesson that is taken away is always and everywhere the choice of the learner.

schools and sports bodies are still trying to teach that “boys can be girls” and that this is not some sort of unfair advantage on the sports field.

it clearly is. it’s not even debatable.

the blank slatists of “gender is just a social construct” are endlessly shown to be liars in every field of athletic endeavor. “male biology and male puberty” are the most potent performance enhancing drugs known.

a group of texas under 15’s demolished the US women’s national soccer team.

look at the size difference. of course this was unfair.

this holds in basically every physical sport.

the below may be slightly dated at this point, but the basic premise holds:

apart from marathon (not an event in HS or NCAA) there is not a women’s world record in track and field that has not been beaten by a (often very young) boy.

most short-distance events see the women’s world champion exceeded by a 14-15 year old.

even the hyper endurance events like marathon where the differences are smaller and the age range stretches (likely because young men are discouraged/not allowed to run marathons for fear of injury), ulimately, the men’s marathon record is 2 hours 35 seconds, over 13 minutes faster than the women’s record)

the spread is huge in the “explosive” events like throwing and high jumping.

It’s why I don’t think they should make as much in Tennis. They play short matches and can’t play at that elite level. The top seeded female might get a few games off the worst guy, but not much more

The Department of Government Efficiency (DOGE) has marked approximately 3.2 million Social Security number-holders for people aged 120 and older as “deceased” as part of ongoing efforts to root out fraud.

DOGE, headed by tech mogul Elon Musk, announced the move on Tuesday after the Social Security Administration (SSA) spent the last two weeks working on a “major cleanup of their records”:

While the table posted by the department shows 3,261,057 number-holders being removed from the “living” count, millions of accounts belonging to people purporting to be up to 159 years old still remain, awaiting review.

“More work still to be done,” DOGE added in its post on X.

Musk called out the SSA for having impossibly old number-holders in its registry in a scathing February post, showing thousands of people supposedly in their 200s, and one even in their 300s:

“According to the Social Security database, these are the numbers of people in each age bucket with the death field set to FALSE!” the DOGE chief and X owner wrote. “Maybe Twilight is real and there are a lot of vampires collecting Social Security.”

A recent Rasmussen poll that asked people if they would “support or oppose having the Department of Government Efficiency do an audit of the Social Security system” found that 59 percent would strongly (41 percent) or somewhat (18 percent) approve of that audit, with only 35 percent opposed it.

Social security experts who spoke with PolitiFact offered two possible explanations for the staggering numbers of accounts that appear to belong to millions of super-centenarians:

Government databases may code someone as 150 years old for reasons peculiar to the large and complex Social Security database.

Improper payments are a longstanding concern for the agency, though they represent a small share of all payments.

According to the International Organization for Standardization (ISO), a missing value for a date is coded as May 20, 1875 — the date that the international standards-setting conference, the “Convention du Mètre,” was held in Paris.

It is necessary to note that the SSA has been automatically stopping payments to account holders over 115 years of age since September 2015, so DOGE is not necessarily stating that the administration has been making payments to the aforementioned 3.2 million accounts.

A report from the SSA’s Office of Inspector General (OIG) states that the administration has not established a new system capable of properly logging death information, resulting in nearly 19 million Social Security numbers for people born in 1920 or earlier not being labeled as deceased.

After President Donald Trump brought up the suspicious database issue in February, SSA Acting Commissioner Lee Dudek thanked him and vowed to continue the investigation.

“I thank President Trump for highlighting these inconsistencies during his speech last night to a joint session of Congress,” Dudek said in a statement. “We are steadfast in our commitment to root out fraud, waste, and abuse in our programs, and actively correcting the inconsistencies with missing dates of death.”

What was your first Computer?

In college back in the 70’s, I worked with punch cards on some timeshare system that the school had, but I have no idea what it was.

My first real computer was an IBM System 34, in the pre-PC days. We coded in RPG II and even had Star Trek as a game on it. It used 8-inch floppies, had 4K of memory, and maybe a 4 MB hard disk (the memories are hazy from those days).

I wrote about it extensively here along with my Mad Men shennanigans about sex and drinking at work before the cancel culture, MeToo and the other bullshit that took the fun out of work.

People are always bragging or taking credit for jobs they should be doing anyway, like this:

Here’s a post generator that makes up stuff for you (link below). I put random stuff in it to get this:

.

You put anything in and pick the level of cringe that you want. It even adds (I guess) fake people who liked it to give you cred when you post it.

Go ahead and punk LinkedIn

History lesson, Democratic Socialists took over Germany in the 30’s. That created the role model for the propaganda machine that is today called Social Media. They used to be known as Nazi’s, unlike the throwaway term used for anyone you don’t like on the Internet now.

Since the Internet is forever, here is the link to them being overlords and believing that they are part of the dictatorship with Google and Meta/Fake book.

PayPal couldn’t help their liberal selves when the over stepped boundaries with the now well known $2500 speech police fine they were to levy per incident.

After massive push back and account cancellations, the excuse “It was misinformation” came out. That is PR spin for we effed up and are trying not to lose all of our money. It’s been walked back faster than grease through a goose.

The updated policy prohibits users from using PayPal for activities that:

“Involve the sending, posting, or publication of any messages, content, or materials that, in PayPal’s sole discretion, (a) are harmful, obscene, harassing, or objectionable … (e) depict, promote, or incite hatred or discrimination of protected groups or of individuals or groups based on protected characteristics (e.g. race, religion, gender or gender identity, sexual orientation, etc.) … (g) are fraudulent, promote misinformation … or (i) are otherwise unfit for publication.”

In an update to this story, PayPal is now saying that they have no such policy and that the notice about the AUP update “went out in error” and “included incorrect information”:

However, when contacted, a PayPal spokesperson said that the Acceptable Use Policy notice went out in error and that the company will not fine users for misinformation.

From Legal Insurrection

Want to see what lying is in PR speech? Here it is:

Well, we grew up with first amendment rights as did our forefathers and at least half of the nation wants to remain free.

The founder calls BS.

They believed they could do it or it wouldn’t have gone through their legal and communications department. Both should be job hunting this morning. Their politics over ruled logic and economics.

Gillette pulled this in the form of male bashing and it cost them $9 Billion. Good luck PayPal.

When you only read things that confirm your bias, it’s a real surprise when the real world doesn’t agree.

Get woke, go broke.

Update: They are almost certainly lying

When I worked in Boca Raton, my collegues were mostly guys in their 20-30’s, trying to make it in the computer industry. I am not naming names to protect the guilty.

We’d go to lunch together and have pitchers of beer, a good time and then go back to work. We were single, well employed and for the most part, presentable to good looking.

One of the lunch spots/watering holes was Tom’s Ribs next door.

On a particular lunch outing, one of our guys invited the editor and some writers of the National Enquirer. This was the 80’s so their reputation was near or at the bottom for truthfulness.

We enjoyed the best ribs in the South (Florida only) and numerous pitchers of beer. I was the PR department where we worked so I bonded easily with them even though we were in different industries.

I was used to reporters being heavy drinkers, but not on the day they had to close the current edition that day and it was only half written.

I chanced to ask the Editor how he was going to fact check his story (something all journalists used to do) in time to get the publication out by deadline. Here it is….he said, we don’t have to worry about the facts. He waved his hand in the air as if he was batting the truth away. The worse things we publish, the more they read. Everyone loves a train wreck and that’s what the Enquirer wrote about.

We all had a good laugh and we went back to the computer world and they went back to the tabloid world and got their edition out on time. The Enquirer was like pro wrestling. We knew it was fake, but watched it anyway. (Now, they get it more correct than the MSM and break actual stories that the rest of the media jointly buries).

I learned a valuable lesson. Even though I worked with the media for a living, I realized that those behind the words are human also. Some care about the truth and others care less. Also learned was that the media has control over some people. In other words, they believe whatever is written, like my son-in-law from Portland who watches NBC and CNN and believes them.

They as a group be-clowned themselves starting with the Clinton-Lewinsky affair in the Oval office, got worse under Bush and gave away any credibility after 2008.

Sharyl Attkisson has a summary of their mistakes. She is the media reporting on them.

It is quite the list. Before you end it, you’d realize just how little you trust the media after watching them blatantly fabricating the truth.

This brings me back to the lunch. The reporters today, care as little about the facts and the truth as the drunk Enquirer writers that day eating ribs. Both laugh at the truth and the integrity of their jobs.

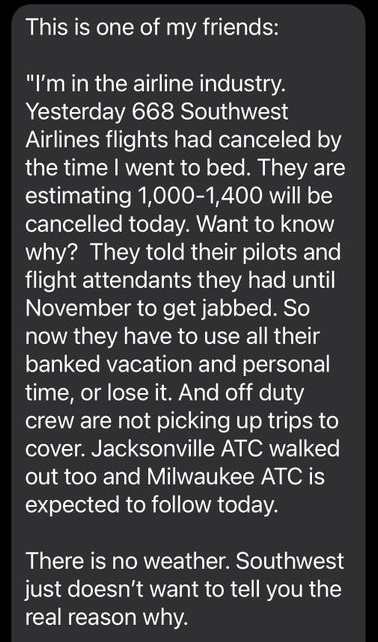

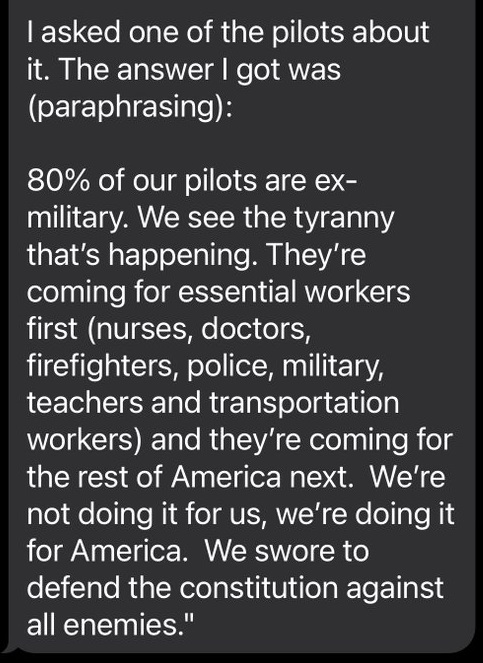

Southwest Airlines cancelled 1400 flights yesterday. They blamed it on weather and other things. No other airlines cancelled flights because of weather. Air traffic controllers gave them the flying fickle finger of fate also and aren’t showing.

It just came out that 200 members of Congress used Ivermectin instead of the jab, hypocrites. Do as I say, not as I do.

From Social Media:

But, I’m retired so everyday is Saturday for me. I don’t have deadlines or conference calls or personnel issues today. Man I don’t miss work.

I don’t miss Facebook that went down yesterday. I didn’t even know it until I read about it. I’m glad to have that ball and chain out of my life also.

I have a brother-in-Law who is retired not by choice, but defined his life by his job. He doesn’t know what to do. I feel sorry for him. Life is much greater than your job.

For now, I’ll pet my dog and enjoy what comes next.

I have been a huge Star Trek fan since TOS. I’ve met some of the actors at conferences for work.

I went to the Star Trek Experience at the Vegas Hilton. It had all the props from all the series in timeline order. There were 3 ships hung above. One was the NCC-1701, there was either the Voyager or Excelsior and I think a Klingon Bird of Prey. No matter, the props were good enough.

I lived each episode as I went down the display case. The actual phasers, tri-corders, costumes and ample descriptions. It took me hours to get through.

Later, they added a Borg exhibit and you get to experience 4D assimilation.

I still have a Tribble at home.

If they would only give me a replicator I’d be in heaven. They probably shouldn’t give me a phaser because I couldn’t promise to keep it on stun for some people.

Activate:

To make carbons and add more names to the email.

Advanced Design:

Beyond the comprehension of the ad agency’s copywriters.

All New:

Parts not interchangeable with existing models.

Approved:

Needs revising

Automatic:

That which you cannot repair yourself.

Channels:

The trails left by interoffice emails.

Clarify:

To fill in the background with so many details that the foreground goes underground.

Conference:

A place where conversation is substituted for the loneliness of thought and the dreariness of labor.

Consultant:

Someone who borrows your watch to tell you what time it is and then walks away with the watch.

Forwarded For Your Consideration:

You hold the bag for a while.

FYI:

Found yesterday, interested?

In Conference:

Nobody can find him/her.

Let’s Get Together On This:

I’m assuming you’re as confused as I.

Note & Initial:

I’m not taking the fall for this myself.

Policy:

We can hide behind this.

Please See Me:

Come down to my office. I’m lonely.

Top Priority:

It may be stupid but the boss wants it.

We Are Taking A Survey:

We need more time to think of an answer or we can’t find anyone willing to be responsible for this.

Will Advise In Due Course:

If we figure it out, we’ll let you know.

“The price one pays for pursuing any profession or calling is an intimate knowledge of its ugly side.” – James Baldwin

Someone said find your passion and you’ll never work a day in your life. This is not true. Sooner or later we become victims of routine or more likely other people will make your job a pain.

This is the ugly side. At some point even Michael Jordan had to retire, but he still can’t go to a restaurant without people bothering him.

Enjoy what you have and be glad you get to do it.

It’s not just older men, it’s older people and little kids. Art Linkletter said that kids tell the truth and older people just don’t give a s&!^ anymore.

“Meetings are indispensable when you don’t want to do anything.”

– John Kenneth Galbraith

We’ve now found out during Covid that in person meetings are not necessary. Actually, most of us knew that from sitting in them and wishing we were dead or anything to not be there.

I do know a few people that love meetings and live for them. I think they don’t want to work, or it’s the place they think they can actually wield power. I avoid those people so I don’t have to go to their meetings.

I’ve written before why Meetings are a waste of time, and how to avoid them.

As an introvert, I loathe meetings. My rule was that if there were anymore than 5 people nothing was going to get done.

Avoid them at all cost. They are a time suck and we’ve now proven that you can get work done without them

When you do things because they are easy or the easy way, life will be hard in the future. When you do things that are hard, life will become easy.

I remember in my early working days when I was busting ass on a Saturday. A friend of mine was giving me a hard time about working while he was on his way to Hawaii because he only worked 2 weeks a month (he was a stewardess – his words). He was flying there for free because he worked for the airlines.

I knew that I was making a short term sacrifice for a long term gain. I couldn’t afford the trip both in terms of money or time off.

A few years later, he decided not to serve cokes in the air for a living, but had wasted 15 years of working experience. I had committed to getting ahead early in my career to enjoy my time later in life. That required me to work hard when I was younger and sacrifice some things.

Now, I go where I want, when I want. I’ve long since retired and my friend is still catching up and will be working for a long time. I can afford a ticket to wherever, usually on frequent flyer points. Life is a full circle.

I’m not a fortune teller, but life is short and there is a time for work and a time to reap the rewards of that work. I knew that early and instead of living for the moment I had to work hard and sacrifice to enjoy the fruits of that labor.

We all learn lessons in life, but the are eerily similar. Few are sports stars, win the lottery or inherit their wealth. You need to work tenaciously, suffer from some hard knocks and learn from your experiences. I knew way back then that goofing off early in life when you should be building the foundation for your life was the right decision.

I decided not to rub it in with my friend now that we are on the other side of the equation. He is suffering enough and it’s just not worth it to me. The results speak for themselves.

Build relationships because people work with the people they know they can trust.

People generally want to do their best. They want to succeed and will bring others along with them.

I have worked with people who trusted me and I know that even though I always gave it my all, I’d give more for those who I knew I could trust. Conversely, while I didn’t work less for those I didn’t trust, I certainly didn’t prioritize them in my time or task management.

People who went out of their way to do me harm I stayed as far away from as I could unless it wasn’t possible. Even then, I was wary of them to the point that I didn’t offer to help when I could at times because I was wary of retribution or motives.

I can’t be that different than anyone else.

Build trust and people will trust you back. Be trustworthy and others will notice.

No one would wish what happened to us with the China/Wuhan/Covid-19/Kung flu/Corona virus this year. I wonder if there is any silver lining?

WE’VE LEARNED THAT YOU DON’T HAVE TO BE IN PERSON AT WORK

First, the essential workers should be commended. Those putting their life at risk for the rest of us or to keep us able to stay away but help keep the economy going do need to be there. They don’t get thanked enough and deserve more accolades than they are getting. I can’t list them all, but you know who you are as do we, especially when we go out or are in need and you are there.

There are a group of desk jockeys that can work from anywhere, including home, the coffee shop or anywhere that has WIFI. Many companies are still getting along just fine without everyone in their cubicles or open office space being babysat by next level of ladder climbers and wannabees.

Yes, some of them are goofing off, but they goof off at the office also. They self-sort themselves out of their jobs after a while anyway. The other workers know who is carrying their load and who is carrying a load of bullshit without them being there.

We have been forced into a higher level of trust to get the job done. I’ve worked for some who didn’t trust their employees if they weren’t at their desk. If you treat people like grownups they will be. If you treat them poorly or like monkeys, like managers I’ve had they will eat bananas.

Now, those who want to work at home or remotely had the chance to prove that they could get the job done and don’t have to go into an office to do the same thing.

For introverts, this is a blessing. They don’t have to be sentenced to the jail of in person meetings or having to have their day ruined by HR regimented nonsense that can be done in non-critical hours.

PRODUCTIVITY

This is a unique time to get more work done, or to refine our work habits. See above about goofing off in the office and you have now eliminated water cooler BS sessions, meaningless meetings that can be done on email or chat and time to actually concentrate.

I know those in sales have to talk, but if they concentrate more on selling, they too will be more productive. A lot of them are too chatty anyway.

The USA works more than other countries and it appears that we like to work. You can tell by how much we’ve achieved, but also the lack of vacation we take vs. other countries. Hey, but how many countries have landed a man on the moon?

We have the opportunity to open up (re-open up) and unleash the greatest economy and workforce that has ever existed. There are people dying to get back to work that may be furloughed. I only hope the politicians haven’t put onerous rules in place that hurts the economy and the ability for small businesses to thrive.

TRAVEL

You can now go anywhere you need to if you want. I imagine that travel will be light at first, although some with pent up demand or anxiety will leave as soon as it is allowed. The downside will be the TSA security check lines if we have to stay 6 feet apart. The line will be out of the building and into long term parking.

I read that the bookings for Cruise ships are in high demand, something I just don’t understand. Cruise ships are petri dishes for viruses and have been for a long time. Why you would want to be in basically a jail cell that travels with limited escape time to buy a T-shirt doesn’t seem desirable, but I have friends who love it. They mostly like to eat though and say it’s a cheap way to travel. At least they won’t be on planes for those of us who want to get where we are going and then actually see the country/place we are visiting.

You won’t have to worry about getting stuck in the middle seat for a while on an airplane. That is the designated social distancing seat, like it’s going to matter when you are in a tube for hours and well within the reach of a cough or a sneeze. I love this one as the airlines have made travel less enjoyable year over year. The armrest fight for position will be solved for now.

I imagine there will be a lot of deals at first. Travel costs should be down as well as tourist traps will have good prices to make up for the time we’ve spent in our quarantine jail. Get ’em while you can. There will be less tourists everywhere you go and businesses dying to offer deals to make up for the faux shut down.

BE POSITIVE

One can look at the downside and think that the world is going to end and that we might die from Covid-19. The statistics say that it is mostly in a few concentrated places (NE corridor and elderly care facilities) and affects those with a co-morbidity. The odds are in our favor that we won’t get it or that it won’t be as bad as the media is trying to shove down our throats.

When this passes (hint: watch how soon it passes after the November election is over regardless of who wins) the opportunities to better your life and enjoy some things in the work/life balance that have been either ruined or complicated for us.

Peter Drucker – “So much of what we call management consists in making it difficult for people to work.”

I’ve posted on meetings being a waste of time and management ego’s. Great managers lead and let the employees work and succeed. Mostly, the best managers help their employees grow and advance in their careers. I know I’ve had both types. When I was a manager, I did everything I could to those working for me the opportunity to show what they can do and help them when they fell down.

Unfortunately, most can’t seem to get out of their own way and realize that the best managers surround themselves with a good team and give them the power to do their jobs to the best of their ability.

“If one does not fail at times, then one has not challenged himself.” -Ferdinand Porsche

People need to overcome challenges and problems in life. They are handed to us everyday whether or not we want them. That is just life and maintaining the balance that humans require.

To get ahead, you must step out, take a risk, use your talents and sometimes you won’t succeed. When you do, you get a sense of satisfaction from overcoming or in the case of Dr. Porsche, you start an iconic car company.

THE SETUP FOR THE DISCUSSION

I suppose every generation considers the learning of the next generation as inferior to theirs. If we didn’t, why do millennials eat tide pods? Why do parents talk about how better their education was and how soft they are on kids today? There are many reasons for this including prejudice, standards, government intrusion into the learning system and deviation from what made our education system the one that led to more progress, inventions and breakthroughs than any in the history of man.

We’ve now potentially gone backwards and have therefore failed the following generations.

In working with public school kids, I observe that there are many reasons. People are not equal and some are smarter and learn better than others. Those with two parent families or with a single parent who is highly integrated in the student’s learning consistently outperform those who don’t. The system has gone backwards due to interference from do-gooders, government (over)regulation and unions. Note: that is my observation only. I see kids rise above the system to achieve, but they have to swim upstream. Most can coast their way through.

Conversely, children who learn under Classical Education have an advantage in learning as it is taught to a standard the kids must keep up with as opposed to teaching to the lowest common denominator so no one is left behind, penalizing those who could achieve more.

Further, Classical Christian education is an approach to learning which emphasizes biblical teachings and incorporates a teaching model known as the Trivium, which consists of the three stages of grammar, logic, and rhetoric.

Classical education complements a child’s natural development stages. Young children can memorize information easily. So, in the early years, learning is enhanced by songs, body movement, recitation, and exploration. This sets them up for success in their next stage of learning, critical thinking.

The critical thinkers are what companies want to hire. They look at problems differently and come to the table with better skills for success.

They also have a distinct advantage over the public school system and the below discussion of how we are destroying learning.

WHERE EDUCATION HAS FAILED OUR KIDS

The biggest failure I’ve observed is the Common Core learning system. It threw away the standards of learning that has proved to produce educated kids by introducing a system that borders on the ridiculous.

It was implemented by those we thought were helping us, yet it may have set us back for years.

Behind a lot of this is none other than Bill Gates, a man I’ve met and have mixed thoughts about. Microsoft is far more successful than his support of Common Core.

From the American Thinker, I read this snippet:

But Bill Gates should have felt some uneasiness. Common Core was untested, unproven, and micromanaged by David Coleman, a man with limited credentials but reliably far to the left. Nobody in the business world launches a big new product without years of research and refinement. Instead, Common Core was wrapped in $1 billion’s worth of propaganda and dumped on the country as a fait accompli.

The late, great Siegfried Engelmann, a real educator, was asked what he thought of this approach: “A perfect example of technical nonsense. A sensible organization would rely heavily on data about procedures used to achieve outstanding results; and they would certainly field test the results to assure that the standards resulted in fair, achievable goals. How many of these things did they do? None.”

Did Gates realize that Common Core, supposedly a new and higher instruction, incorporates all the dubious ideas from decades prior? New Math and Reform Math were the basis for Common Core Math. Similarly, Whole Language and Balanced Literacy were rolled into Common Core’s English Language Arts (jargon for reading). Constructivism, which prevented teacher from teaching, has been undermining American schools for decades. Nothing new and higher about these clunkers.

An earlier generation of Gates’s business partners had created so much illiteracy that Rudolf Flesch had to write a book to answer every American’s favorite question: “why can’t Johnny read?”

I don’t hold Gates responsible except for his funding and use of his status to push this, but I hold those who pushed this system on the generation suffering from this learning standard.

The Thinker sums it up like this:

We have to wonder if Bill Gates performed due diligence, that being the care that a reasonable person exercises to avoid harm to other persons or property. In other words, before putting your business funds to work on anything, you should make yourself an expert. That’s what we need in this country: everybody becomes an expert. For sure, nobody should trust the official experts. If Bill Gates had observed that simple rule, he would still have a billion or two he doesn’t have now. And the country would have tens of millions of better educated students it doesn’t have now.

We need to stop this disservice to our kids and have them learn properly, and to learn to think critically.

Here is a video that shows just how far we’ve deviated from the learning system that invented computers, vaccines, technology that has helped mankind and sent men to the moon. Go to 1:24 under Decompose to see how far we’ve digressed.

CONCLUSION

It would seem the dumping common core and putting real learning would be best for the kids. The world is getting tougher and we need to give them every advantage possible.

I love controversial subjects, especially among the sexes. Nothing gets the hackles up quicker than something that offends what you hold close to your heart. I’ve worked with the media for decades and sensationalism is what sells. It’s sex, death, murder, immorality, bankruptcy, divorce and other vices that can be cherry picked to place on the headline. This is not real life, like…..

Ye old workplace.

It is a petri dish of human interaction that has been infected by #MeToo, harassment, incivility, sexism, partiality, affairs and occasionally competent work and results. I’ve already discussed if Men and Women can work together here, and Women now swear more than men, so I found this article and it looked either like a headline maker or a trend. I decided to find out.

Having sat through weeks of diversity training that is beyond boring and is a CYA for the legal department, I’ve been told that you can’t say certain things, act in a ways that could be demeaning or sexually suggestive or anything outside of plain vanilla. I choose to keep to myself and observe. That is why this study caught my eye. The behavior is far outside of my diversity training, yet it goes on unabated.

WHO ARE THE BIGGEST OFFENDERS?

A recent study shows that women are reporting that it is other women who are the most rude and uncivil towards women. It goes like this:

In terms of how it is acted out:

“Across the three studies, we found consistent evidence that women reported higher levels of incivility from other women than their male counterparts,” Gabriel says. “In other words, women are ruder to each other than they are to men, or than men are to women.

“This isn’t to say men were off the hook or they weren’t engaging in these behaviors,” she notes. “But when we compared the average levels of incivility reported, female-instigated incivility was reported more often than male-instigated incivility by women in our three studies.”

THE QUEEN BEE SYNDROME

The article at the link above states:

The phenomenon of women discriminating against other women in the workplace—particularly as they rise in seniority—has long been documented as the “queen bee syndrome.” As women have increased their ranks in the workplace, most will admit to experiencing rude behavior and incivility.

Who is at fault for dishing out these mildly deviant behaviors? Has the syndrome grown more pervasive?

“Studies show women report more incivility experiences overall than men, but we wanted to find out who was targeting women with rude remarks,” says Allison Gabriel, assistant professor of management and organizations in the University of Arizona’s Eller College of Management.

I worked with a female named Sandy. No one was harder to understand or trust as a senior manager than she. My friends would dread working for her and it was a success not to get fired before your term was complete. Everyone tried to get out as fast as they could, or would not seek a promotion just to not work for or with her.

I WANTED TO KNOW SO I ASKED THEM IF IT WAS TRUE, WHAT THEY SAID, PERHAPS NSFW

I like to look at things from the point of view of how would an intellectual view this. Normally, this would entail a scientific study without bias, with control groups and so forth. My observation is that people’s behavior is not scientific when it comes to emotions and I’ve been told by those of the female persuasion that they are more likely to be emotional. I couldn’t argue the point, nor did I care to.

Therefore, I figured that asking some females if this was correct and what they’ve seen at work would be my best estimate as to whether this is true. Please note that some of the comments while stated verbatim are not always complimentary and some are off-color. Commenters: Note, if you get pissed off, these are answers by women to a question I asked about working with females and is the study accurate. If you just want to hate, please go elsewhere as if it’s directed at me, it’s a fart in the wind and that’s how I’ll treat it.

Here are some responses:

Females can be bitchy, catty. other names.

She slept her way to her position.

She got there because of her looks (or tits), not her ability.

She dresses like a whore.

There is one bitch who leans over in front of guys to get her way.

Women are the biggest backstabbers.

Sure there is an occasional guy who bugs me or tries to hit on me, but girls are far worse as a group.

Sure she was nice when she was one of us, but as soon as they gave her a little power, she turned on us like we’d done something to her.

She’s great to work for if you are female. She only promotes women and you can get your way over any guys.

Women here can only manage 2 inches in front of their face. They don’t get the big picture or work towards the company’s goals.

Once you make it clear you aren’t going to sleep with them, the men are much easier to work with or for. The mission and strategy are clear and they can focus on that.

Guys will either just not say anything or will tell you how it is. The girls say something to your face and f__k you over behind your back if you aren’t in their group.

Guys handle success and failure better than the girls I work with. One of them always takes it personally and spends weeks trying to get back at you instead of trying to get work done.

I can never trust what a woman says to me. Guys don’t lie as much or as well as girls do unless they want in your pants.

Women talk too much and I can’t get my work done.

When aunt Flo comes calling honey you better hide from that bitch.

Just get more than one female together in a group and watch the fireworks.

Guys are used to joking, I think they learned it in a locker room or something. They can cuss each other out in a meeting and it’s like a punch in the arm and then go have a beer. A woman will hold something you say to her against you for the rest of your life.

Enough! Most of these I got multiple times, which is why they made the list. I stopped asking because this attitude was overwhelming me.

CONCLUSION

I can only surmise that it is tough for women to work with women. I didn’t give it much thought until I read this study, but it does appear that women are more difficult towards other women at the workplace

In these days of divisiveness, there are some facts based on economics that are hard to refute, even if you don’t want to admit it. I enjoy discussion by people of high IQ and of great wisdom, something the world of Political Correctness is sadly overlooking.

I read a WSJ article on ineffective meetings. It is about the manifesto to end boring meetings.

I read a WSJ article on ineffective meetings. It is about the manifesto to end boring meetings.

This brought back thousands of hours of meetings I wished I could have back or would certainly decline to attend had I realized what I know now. Most of this post is tongue in cheek unlike the WSJ, but I’ll bet everyone wishes they weren’t in so many meetings.

First, let me start out with some quotes I found from The Quote Garden, starting with the one that reminded me most of the meetings I’ve attended:

A committee is a group that keeps minutes and loses hours. ~Milton Berle

To kill time, a committee meeting is the perfect weapon. ~Author Unknown

If you had to identify, in one word, the reason why the human race has not achieved, and never will achieve, its full potential, that word would be “meetings.” ~Dave Barry, “Things That It Took Me 50 Years to Learn”

Our age will be known as the age of committees. ~Ernest Benn

If Columbus had an advisory committee he would probably still be at the dock. ~Arthur Goldberg

A committee is an animal with four back legs. ~John le Carré, Tinker Tailor Soldier Spy

It is impossible to imagine the universe run by a wise, just and omnipotent God, but it is quite easy to imagine it run by a board of gods. ~H.L. Mencken

A “Normal” person is the sort of person that might be designed by a committee. You know, “Each person puts in a pretty color and it comes out gray.” ~Alan Sherman

A committee is a thing which takes a week to do what one good man can do in an hour. ~Elbert Hubbard

A camel looks like a horse that was planned by a committee. ~Author Unknown

A committee is a group of the unwilling chosen form the unfit, to do the unnecessary. ~Author Unknown

If you live in a country run by committee, be on the committee. ~Author Unknown

Could Hamlet have been written by a committee, or the Mona Lisa painted by a club?… Creative ideas do not spring from groups. They spring from individuals. The divine spark leaps from the finger of God to the finger of Adam. ~Alfred Whitney Griswold

We always carry out by committee anything in which any one of us alone would be too reasonable to persist. ~Frank Moore Colby

I don’t believe a committee can write a book. It can, oh, govern a country, perhaps, but I don’t believe it can write a book. ~Arnold Toynbee

There is no monument dedicated to the memory of a committee. ~Lester J. Pourciau

Any committee that is the slightest use is composed of people who are too busy to want to sit on it for a second longer than they have to. ~Katharine Whitehorn

Meetings are indispensable when you don’t want to do anything. ~John Kenneth Galbraith

People who enjoy meetings should not be in charge of anything. ~Thomas Sowell

Usually, the meetings were a way to get other people to do your work for you, or to assign work to others they wouldn’t do or volunteer for were it not for the fact that they were at a meeting. The only time this didn’t work was when I actually needed to get a speaker for a press briefing for an interview with Time Magazine when print media was important. His manager, John Callies then VP of Netfinity or X series at IBM(x86 servers), wouldn’t let the speaker leave the staff meeting stating, “it’s only your job” as the reason. See how manage executive ego’s for more on this. I’d have never imagined having to cancel an interview with what was then an important publication due to an executives’ ego. I’ve seen bad manager moves in my time, but this was top 10 worst of the worst for me. He still ranks as the number one suit I’ve ever worked with. The below meme was how it felt to be in a meeting with him.

Execs have also had meetings in places that they wanted to visit (click on the link to see who it is), and most people knew that. That was a waste of travel time and money for a wasted meeting. There were other reasons they had meetings, but read the quotes at the beginning to find out why said were held.

Avoid training meetings, unless it was a way to be busy during a meeting you want to avoid. This is especially true of diversity training. It is a waste of time (same exact meeting every time every year for the required legal reason) but is more important than almost any other meeting, so it serves 2 purposes. No one will go against diversity training for fear of being politically or legally incorrect. It does allow you to miss another meeting and no one pays attention anyway. It’s an opportunity to get work done while the training is going on in the background. Your attendance is recorded so you are twice as effective as you complete your work, earn your mark for training and ignore the same speech you went through last year all at the same time.

MEETING RULES TO SURVIVE

The best way to deal with a meeting is to avoid it. If you can already have a meeting at a time that the scheduler proposes it or be busy and/or somehow away or out of the office. Teleconferencing kills that strategery unless you can be found traveling, but sometimes it’s unavoidable (see how to get out of a meeting below if you have to go). The people calling the meeting are really only people who want the meeting anyway.

For things to do to avoid meetings or how to goof around during a meeting, go to the link How to goof around at work.

HERE IS MY RULE WHEN TO DECIDE TO ATTEND IF I HAD A CHOICE: if there were more than 4 people, don’t go. Nothing will get done other than resulting in another meeting to have to attend. This is especially true if there are more than 1 executives, as each brings a team of competing players who guarantee the death of productivity.

The WSJ agrees with me, but goes on to say that if it has 17 people, there is no chance anything will get accomplished.

Don’t speak at a meeting if possible. It usually wastes time and extends the meeting length. There are only a couple of people who really have something to contribute, the rest want to hear themselves talk, show off their PowerPoint skills to bore you, or think they are more important if they speak. These show offs can be insufferable, but they offer time to check your email at best while pretending to listen.

This is in the department of redundancy department, but it is so important to note is to be careful when attending because the meeting leader’s purpose is to assign their work to others or get people to do work they wouldn’t do because they can’t decline in public (this is a corporate tradition). This further kills your ability to be productive at your real job. There are some who want to look important by accepting work magnanimously to show off, thinking they were climbing the ladder. Gladly accept their offer as most people have 10 hours of work for an 8 hour day anyway. Only accept it if it produces revenue or if you are the only one qualified to do it, but generally don’t, especially if you perceive it as a make work project.

Especially avoid planning meetings. A meeting to plan another meeting is one to be skipped unless you are the project manager and called the meeting, then you have to do it. Avoid these at all costs. Once nobody shows up, the meeting gets cancelled for email updates, which is a far better use of your time. As my grandfather said, they are as common as pig tracks and as useless as teats on a boar hog.

Avoid staff meetings. These are like planning meetings, but they occur regularly and when you miss one, nobody really cares (especially if there are more than 4 people). Only attend them occasionally as you work with these people everyday anyway, it’s not like you don’t know what is going on. Email your boss on a regular basis with your activity and you can plan something more productive during that time.

HOW TO GET OUT OF A MEETING

The tongue in cheek part really goes here. I’ll bet there are folks out there far more creative about this than me.

My favorite methods are to have a customer who needs you. They are your business and that overrides almost everything. Even your boss can’t deny this.

Pre-plan an emergency. I occasionally had another employee phone or knock on the door to call me out (email or text isn’t as good as that is not public enough) to get you out of a meeting. The trick is to never return. You’ll get the notes anyway, I promise. Since I worked with the press and analysts, I sometimes had a co-worker say that a reporter needed me right now. They were my customer and no one could say no. Many times there was no real emergency even if the press did call, it was the best and most efficient use of my time to leave the meeting so as to be actually working instead of being at a meeting. I usually dealt with the press immediately unless I had to do some digging to get back to them.

Attend meetings by phone if possible. You can always put the phone on mute and get your real work done, or surf the web or watch TV, which is usually just as productive. It’s easier to go to the bathroom, which brings me to…

Go to the bathroom. Offer to get a water to others when you go, then take as much time reading the sports page in the stall as you can. You are just as productive as listening to someone prattle on about their project.

Send your meeting information in by proxy. See above where someone is willing to talk. Give them your results or input so you don’t have to be there.

I realize that some meetings are necessary, so I understand that it’s the only way to get some things done. For the other majority of the time, see above.

The best meeting is a hall meeting. You run into the person you need help from and in 5 minutes, you’ve explained your need, what they can do and your time frame for doing it. Problem solved.

I also recommend having meetings with introverts and/or men. They don’t like to talk much (most of them) and want to get it over as quickly as you do. Attire requirements are less of a priority as is small talk.

Here is the net net, don’t go to a meeting if you don’t have to, get out early if at all possible and above all, don’t speak unless you have no option. Consider it a victory if you don’t attend, or a minor victory if you have to attend but don’t come out with anyone else’s work. You are a complete failure if you open your mouth and double your workload on something that is not tangential to your job or career. Enjoy your job more by having the time to actually be productive.

The brilliant John Hawkins presents the facts about this subject. It is to be the 2014 top priority from our executive branch. Readers should evaluate the facts and judge for yourself if this is good for the country or not. Park your ideology at the door (regardless of its source) and think through the argument. Your beliefs are yours, just make sure to check with history to see what information it supports

The truth is that income inequality is of minimal importance in a nation like America, where so many people already move between classes, where the poor are doing so much better than they used to, and where our poor already do so well compared to the rest of the world. “Among children from families in the bottom fifth of the income distribution, 84 percent of those who go on to get a college degree will escape the bottom fifth, and 19 percent will make it all the way to the top fifth.” During the Great Depression, more than 60% of Americans were living below the poverty line. Over the last 50 years, that number has generally ranged between 12%-15% — and even that dramatically overstates the number of poor Americans because it doesn’t take into account government assistance that’s being paid out. On top of all that, liberals get so angry when people point out that more than 80% of poor Americans have cell phones, televisions and refrigerators while “most Americans living below the official poverty line also own a motor vehicle and have more living space than the average European.” Yet, they don’t take into account the fact that almost half of the world’s population still lives on less than $2.50 a day. In other words, if you are poor, you can live better and have more opportunity to advance in America than you will anywhere else. That’s why immigrants all across the world still want to come to this country.

1) The higher the government mandated minimum wage/living wage, the more people it prices out of jobs: When you force businesses to pay people more than they can return in value with their work, companies tend to respond either by hiring better quality people, replacing the jobs with automation, moving the posts overseas or by looking for opportunities to get rid of the positions entirely. The higher the wages and benefits the government insists on, the more stagnant it makes the labor market for the people who need to build their skills the most. If your goal were to deliberately put as many young, unskilled single mothers out of work as possible, the best politically feasible way to do it would be to jack the minimum wage up into the stratosphere.

2) It emphasizes making people more comfortable, not helping them succeed: There is no shame in taking any honest job, but you’re not supposed to make a living pressing the button that drops the fries into the grease at McDonald’s. If you work long enough at an entry-level job to worry about raising the minimum wage, you’re failing your family, your society and yourself. Instead of encouraging minimum skill workers to demand that the government force businesses to give them more money than they’re currently worth, we should be encouraging people to build their skills and move up, move on or start their own business. Want poor people to be eligible for more education or training? Want to give them micro-loans? Want to make it easier for them to create small businesses? Those are policies that make poor Americans more valuable. That’s good for them and the country. On the other hand, trying to redistribute income ultimately brings everyone down, especially the poor Americans who lose their drive after becoming dependent on it.

3) The more government becomes involved, the more it stagnates the economy: As John F. Kennedy said, “A rising tide lifts all boats.” The stronger the economy is, the more jobs it creates and the more everyone — poor, middle-class, or rich — benefits. How do you make the economy stronger? You keep the government small, taxes low, and regulations light. That’s a proven formula that has worked time and time again. On the other hand, if you want to constipate the economy, you make the government bigger, increase taxes and pour on the regulations. How did that latter set of “solutions” work out for Detroit?

4) The more the government focuses on income inequality, the harder it is to get ahead: As Thomas Sowell likes to say, “There are no solutions; there are only trade-offs.” You can see this very clearly with Obamacare, where a few people are getting subsidized care, while tens of millions more are losing their health care and paying considerably more to make up for it. It works the same way with income inequality. Want to make Wal-Mart pay all its employees twice as much? Then that means all the poor Americans who shop at Wal-Mart will have to spend more of their limited incomes to pay for it. Want to give more tax dollars to the poor? Then the rich and middle class will have to pay more in taxes. So, the moment that poor American is making enough money to get into the middle class, he’s hit with a bigger tax bill that makes it harder for him to ever get ahead. In other words, the more resources we put into “helping” the poor, the harder we ultimately make it for those very same people to ever permanently escape poverty and live the American Dream.

5) It ignores the real causes of poverty: The real causes of lasting poverty in America are not greed, the rich, racism, America being “unfair,” or any of the other excuses that you hear so often. Instead, the harsh truth that so many people don’t want to hear is that if you stay poor in America, it’s usually because you made bad life choices. Via Walter Williams, here’s what you have to do in order to avoid poverty in America.

“Complete high school; get a job, any kind of a job; get married before having children; and be a law-abiding citizen. Among both black and white Americans so described, the poverty rate is in the single digits.”

Instead of lying to destitute Americans and telling them that the rich became wealthy by stealing the money that the poor never had in the first place, why not tell people the truth? Yes, it might make some poor Americans feel bad, but do you think welfare, food stamps, and living in a housing project do wonders for people’s moods?

HOW IT STARTED

This story actually began with the unplanned running aground of the Mercedes I in Palm Beach. It desecrated the private holy grounds of the hoity toity for over a hundred days in late 1984. They eventually towed it away and made an artificial reef making almost everyone happy.

About the same time IBM introduced the PC-AT, billed as the most powerful personal computer ever built. It had one problem though as internally sat a 20 MB disk drive made by CMI. It was based on stepper motor technology and it both failed at alarming rates and was as slow as cold honey. It was that flaw which helped give birth to the drive aftermarket in the PC industry and caused one of the biggest black eye’s to the PC’s reputation.

CORE INTERNATIONAL TO THE RESCUE

A small storage company in Boca Raton – the home of the IBM PC saw the obvious problem and created a marketing campaign which recalled the IBM drive. It then sold you a 40 MB drive made by Control Data Corporation and rebadged as CORE product for $2,595, gave you a $1000 rebate and ran an ad claiming it was going to build an artificial reef out of the CMI drives (you can buy gigabytes now for less that $100). CORE was making over 100% profit so the perception of value is greater than reality. The users still paid one of the highest cost per byte of storage possible.

Here is a portion of the ad which created a sensation in the print media, as both IBM and the PC had been infallible up to this point.

Here is a portion of the ad which created a sensation in the print media, as both IBM and the PC had been infallible up to this point.

PC MAGAZINE CATCHES ON

At this point Paul Sommerson, Bill Machrone, Bill Howard and other writers contacted CORE and asked for pictures of the reef being built. The company owner confided in me that he had a contract to send the drives back to CMI for a rebate and to not lose too many, we staged the entire event. We took his boat, the MEGABYTE out of Jupiter (not Boca) and made it look like we were really dumping the drives into the water. I’m sure the Nanny state EPA would have been all over us had we really done it, but the rest of the story is that we only dumped the drives in the picture (note the false bottom). We tried hard to drop a drive on a string while posing with the box in the picture, but all that produced were lame results. I finally convinced him that we needed to actually throw some drives overboard and that one shot is now etched into PC history. It was the last picture on the roll of film (if you remember film). We tried fishing for sharks after the shoot to put a drive in one of their mouths for the table of contents. We had one on, but it bit through the line and we ran out of time.

The film was immediately Fed-ex’d to NY as they were on deadline for what is known as the Fire Ax issue. The title was “Is Your PC Safe”, but there was a fire ax coming down on a PC-AT and the picture was in both the table of contents and the article.

It should be noted that neither CORE nor PC Magazine was trying to attack IBM products. The owner at CORE was excellent at marketing and had big balls to do this stunt. It paid off handsomely both in dollars and visibility. PC Magazine was at the height of their prowess as journalistic leader of the PC industry. Kudos should be given to Bill Machrone for approving a story that would never have a chance at seeing the light of day in this day and age. He was a visionary at the publication. IBM did themselves in by releasing a defective product and not being nimble enough to deal with the issues.

Both parties were able to take advantage of the arrogance (some say ignorance) on IBM’s part for not ensuring quality control of their product and suppliers. Further, the moribund IBM PR machine, having used their death grip to the throat of PC journalism to direct results they wanted (because they were the 800 lb. elephant in the room) didn’t know that the journalists were ripe for this. They never saw this coming and were ill-equipped to deal with it. The result was that both the reputation of the PC and IBM PR was tarnished.

It should be noted that the Wilmott’s were related to the Ziff’s, who owned PC Magazine. It took me 30 years to make that connection,

THE AFTERMATH

As I mentioned earlier, the boom of peripherals was starting and this poured gasoline on that fire. CMI went out of business after losing their contract with IBM and CORE shipped hundreds of drives while becoming famous.

I personally conducted many interviews discussing drive technology and the stunt (if I recall, the story became far better than the actual event) and the owner had to move his boat. He had rented a slip from an IBM’er in Boca, but due to the kerfuffle he was asked to find another docking space.

IBM had a PR nightmare on its hands now. I’m told that Lou Gerstner’s personal speech writer was called in to clean up the mess. CORE (meaning me as I handled all of PR by this point) got years of mileage from this event. I developed relationships with the leaders in PC journalism as they were happy to have a person to talk to rather than an army of IBM suits that outdid the White House press corps in obfuscation. We even took a drive to trade shows and put it into a fish tank with fish. Everyone in the industry knew about it and we even had hats made up saying things like:

My drive won’t stay up, I built the PC that IBM didn’t, My Drive is bigger than your drive and others.

We gave away thousands. In fact I think we invented the show hat give away in the mid 80’s (one time while leaving the show, we saw a drunk bum outside a convention center at with a CORE hat on).

The owner made show participants suffer through a sales pitch they didn’t care about, but the rest of us just gave them away.

The owner made show participants suffer through a sales pitch they didn’t care about, but the rest of us just gave them away.

EPITAPH

It is funny to me that I was hired by IBM to do PR for them 14 years later, and even did a stint in the PC division. I wonder if they had known it was me that helped cause one of the great PR nightmares for them, would I have gotten the job?

IBM had dropped to 6th place in PC’s by then and the PC PR department was led by two nincompoops when I got there (Mike Corrado and Ray Gorman). I always chuckled when the story came up at IBM and enjoyed the looks on their faces as they found out my part in this event. I was never involved with anything this creative while doing PR at IBM (see the moribund part), although I used some tactics from this event to be successful, so long as I didn’t tell IBM communications “leaders” about it until after the fact.

Now, did anyone read to here and notice that for a while I misspelled artificial in the title? It was a PR project for you.

In a WSJ article today entitled, “Men and Women at Work: Unhappy, But Productive“, I couldn’t help but recall some observations I’ve made over the years at multiple companies in many situations. If you are the PC police, save your hostilities as most of this is common sense.

The article states this:

When women and men work together on teams, the results are good for business—but they don’t enjoy it much.

That, at least, is the experience of employees in one company, a large US professional services firm studied by economists at Massachusetts Institute of Technology and George Washington University.

Researchers looked at eight years of the firm’s revenue data and employee surveys, measuring satisfaction, cooperation, morale and attitudes toward diversity. That included data from offices or teams that were entirely male or entirely female, along with data from teams that were more evenly mixed.

On surveys, individual employees reported higher levels of job satisfaction when they were on teams that were mainly staffed with people of their own gender. Those on more diverse teams reported lower levels of happiness, trust and cooperation–consider this Journal essay on what men don’t know about women at work – although revenue figures showed they were more productive and better performing—by a lot.

“People are more comfortable around people who are like them,” says study co-author Sara Fisher Ellison, of MIT.

It may be that members of homogenous groups “socialize more and work less,” Ellison notes. Mixed groups may lack social capital, but varied perspectives and skills may help a unit perform better. The researchers posit that shifting an all-female or all-male team to a coed one would increase revenues by 41%.

Also, researchers found that workers seemed to appreciate the idea of a diverse workplace more than they liked diversity in practice. According to employee surveys, workers gave gender and racial diversity high marks for boosting morale, trust and employee satisfaction, but those who actually worked on diverse teams tended to report lower levels of those traits.

My take so far…..

This prompted some thoughts that many have made about the differences between men and women. It’s likely that women have kept men from wiping each other off the planet in the adult version of kill the man with the ball, or who wants to be king. Conversely, men have killed each other over a woman (OK, women have killed over men also to a lesser degree) but that isn’t the same as competition in the workplace.