There must be some people who are afraid of him running again. They are friends of Epstein, who didn’t kill himself. He must be a threat to their power base and them hiding the evidence and the client list at the Island.

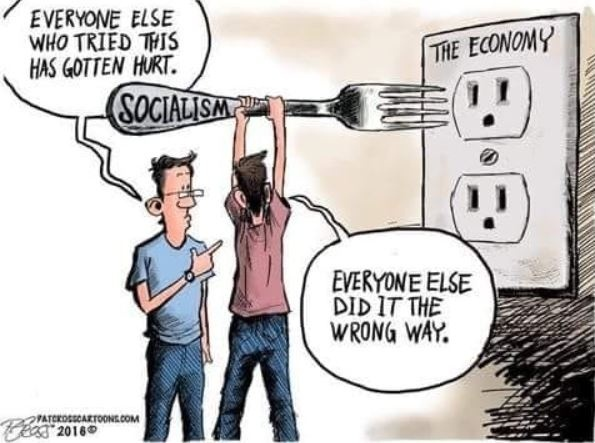

They want power and control. We know how that eventually works out. In 2 short years, the best economy ever, for most of the world just went in the toilet.

Naturally, those currently in charge are claiming that Constitutionalists are Fascist’s. Let’s look at one of the real fascists to see. After all, politicians are doing what they say the other side is doing as they get up on the alter of high holiness.

By death, I mean the first time it was allowed to be fully implemented and the world can see the destruction of deficit spending. It is how it will end when Keynes is allowed to play out without interference.

I’ve always wondered what could happen in a pure Milton Friedman or Keynes economy. It’s been more Friedman since the failure of the The New Deal, a Keynesian try and spending your way out of a depression. Of course WWII and a good economy actually did it, supporting Friedman, but it hasn’t stopped many presidents since then of trying it. Friedman’s capitalistic ideas brought more freedom and prosperity than the current philosophy

I don’t think they believe anything about Keynesian economics other than the part about government spending, because the Keynesian politicians use to to launder money back to into their pockets.

We know the New Deal (like the Green New Deal) failed and just spawned other failures like welfare, the Great Society and now Build Back Better.

At least we know how it turns out in a Keynesian model now, Build Back Broke. It gives power to the few and the government, which is not how our republic succeeds.

Everyone can see our economy being destroyed. Gas prices, food shortages, wars, inflation, border security…all there in back and white. They are socialistic policies that have a zero record of success.

The motto of the interloper now serving in the White House is “Build Back Better” – and the trillions to “build back” is an updated version of the New Deal on steroids. The Dems spend to a new level of excess which, for them, is ecstasy. In fact, a better name for their spend, spend, and spend more programs should be “Excess Ecstasy Exhilarates.” The foundation of the New Deal was found in the economic theory of John Maynard Keynes. Keynes was a British economist who developed the theory of ‘deficit spending’ – the idea that the government going into debt would jump-start the depressed economy which, then, would experience reinvigoration. There would be more employed, tax-paying citizens as well as corporate profits which would, in turn, restore the needed balance to the federal books. The deficit spending would restore a solvency that was lost due to the Great Depression.

In practice, this did not work out (unemployment was still in double digits throughout the 1930s), but because of the passage of the Wagner Act, which made it easier for workers to organize into unions, and because of the use of the radio for the well-known “Fireside Chats” – a real novelty in American politics which intensified public support for FDR – and because of residual anger towards the Republicans who had maintained power throughout the 1920s and were thus assumed to be the ones who had caused the Depression, Keynesian economics became the go-to model for economic policy in the United States for all decades since that time.

However, the Keynesian model has been weaponized under Build Back Better in a most sinister way. The present shift is to make us more amenable to the globalist fantasies gaining popularity in recent decades to ensure a transition towards world governance and a cooperative world economy (rather than a competitive one) under the cloak of “meeting needs” and “sustainability.” These two concepts are key pillars in a document written and published by the United Nations called Agenda 2030. Although the original United Nations Universal Declaration of Human Rights of 1948 stressed the need for individual rights after WWII and promoted those rights in nearly every sentence of that document, the present document – Agenda 2030 – only refers to rights in one of the ninety-one sections: Section 19.

Instead of rights, needs are emphasized. This is consistent with the Communist Manifesto authored by Karl Marx and Friedrich Engels in 1848. A key principle in that document is “from each according to his ability, to each according to his needs.” The actual needs of people would be the uppermost goal of envisioned communist society rather than ideas like rights, freedom, responsibility, property ownership, pursuit of happiness, or even security. The new communistic premise is that if needs are met then people will automatically experience security and happiness and will not need the abstract fluff of such bourgeois, outdated, and elitist ideas as rights, freedom, or ownership. Further, the meeting of communist needs must be based on sustainability. If we run out of energy, clean air, or water at some point in the future, we would then not be able to meet peoples’ needs. Therefore, plans and actions to sustain all the materials and planetary conditions that will keep us from running out of the natural resources are “necessary” – even if that means enslavement and tyranny. ‘Sustainability’ works in tandem with the ‘meeting of needs’ as a combination that is a cornerstone for a new world governance policy.

The Build Back Better plan superficially appears to be an updated and extravagant Keynesian or New Deal-style spending program, but the endgame is not economic recovery that forever establishes federal government dominance over the states in the socio-political realm. Rather, this BBB is the connection of an enlarged federal government and authority with a depreciation or elimination of U.S. sovereignty in favor of global, communist-style governance. But as if the endgame were not sinister enough, we see this updated Keynesian expansion of expenditures is not a result of economic collapse due to a devastating Depression, as was the justification in the 1930s.

Rather, simultaneously with expanded spending, the goal of the BBB plotters is to weaken the economy and usher in economic and socio-political chaos and mayhem. The southern border hands-off policy is literally facilitating the entrance of millions of unvetted persons. By limiting or eliminating natural gas and oil production in the territorial U.S. under the guise of protecting the environment, the feds incentivize other countries to expand their production of these energy sources. That production, which still means higher energy prices here in the U.S., has an equally negative effect on the world climate as fuel production in our country. But the brooding minds behind BBB want to see inflated prices. They want to see shortages. They want to see racial unrest. They want to see upsurges in crime as new theories of law inform the release of repeat offenders and shorter sentences to destabilize society. The BBB autocrats want to see a society that increasingly identifies as LGBTQ because this radical individualism weakens the social fabric. They want to see Chinese fentanyl imported to kill our citizens who are weak-minded and susceptible to drug use.

Thus, despite its resemblance to the New Deal, the BBB’s so-called governance (properly called betrayal) is at the front end linked to global health, green initiatives, and “interdependence” as an excuse for diminishing U.S. sovereignty. Initiation of these policies was not to combat financially depressive conditions but rather designed to undermine the freedoms and economic viability of the U.S. This might be likened to prescribing chemo to a patient who did not have cancer, and then, in order to justify the perverse treatment plan, injecting the patient with cancer cells in order to justify that plan. The goal of the sinister and aberrated “plan” would not be the recovery of the patient and return to normal living, but to place the “cured” individual into custodial care rather than independent living. That is the equivalent of a United States with diminished sovereignty in a world governance system.

It’s not that the Keynesians aren’t smart, nor poorly educated, nor bad economists (at least they studied it to make their economic position), rather it is that they are not students of history. I may have to argue that they are bad economists later though as it has yet to work and is failing again.

So what kind of Keynesian world are Bernanke and the other wise ones in Washington shaping for us?

Keynesians see a depression as a lack of aggregate demand — as opposed to Austrians who know a depression is the required cleansing of the malinvestments created by the preceding boom of the government’s making. Policy makers, following the Keynesian playbook, enact policies to stimulate aggregate demand and offset the fall in private investment. On the fiscal-policy side, Keynesians advocate higher government spending. On the monetary side, they insist on lowering interest rates to zero if necessary.

The world has recent experience with attempts at resuscitating a bubble economy. The Bank of Japan cut interest rates six times between 1986 and early 1987 and all that new money caused the Japanese economy to bubble over. As Bill Bonner and Addison Wiggin write in Financial Reckoning Day Fallout,

the problem with all money is that it is as fickle and unreliable as a bad girlfriend. One minute she goes along with the flow. The next minute she turns silly and bubbly. And then, she gives you the cold shoulder.

The prolonged period of low interest rates created one of the largest domestic bubbles in the world. For a brief moment in 1990, the Japanese stock market was bigger than the US market. The Nikkei-225 reached a peak of 38,916 in December of 1989 with a price-earnings ratio of around 80 times. At the bubble’s height, the capitalized value of the Tokyo Stock Exchange stood at 42 percent of the entire world’s stock-market value and Japanese real estate accounted for half the value of all land on earth, while only representing less than 3 percent of the total area. In 1989 all of Japan’s real estate was valued at US$24 trillion which was four times the value of all real estate in the United States, despite Japan having just half the population and 60 percent of US GDP.

“The Japanese asset bubbles were identical to other asset bubbles in the sense that they were essentially inflated by credit,” writes Asian bank regulator Andrew Sheng in his book From Asian to Global Financial Crisis.

Banks lent to highly leveraged developers to buy real estate against inflated collateral values, which then fueled the bubble further. Asset prices bore no realistic relationship to their return on capital, particularly since cost of funding was exceptionally low. The minute the credit stopped, the bubble began to deflate, and the main victims were the banks themselves.

After the bubble popped in Japan, that government pursued a relentless Keynesian course of fiscal pump priming and loose fiscal policy with the result being a Japan that went from having the healthiest fiscal position of any OECD country in 1990 to annual deficits of 6 to 7 percent of GDP and a gross public debt that is now 227 percent of GDP. “The Japanese tried to cure an alcoholic with heroin,” writes Bonner. “Now, they’re addicted to it.”

Japan’s monetary policy was to aggressively lower rates to .5 percent between 1991 and 1995 and has operated a zero-interest policy virtually ever since.

Between 1992 and 1995, the Japanese government tried six stimulus plans totaling 65.5 trillion yen and they even cut tax rates in 1994. They tried cutting taxes again in 1998, but government spending was never cut. Also in 1998, another stimulus package of 16.7 trillion yen was rolled out nearly half of which was for public-works projects. Later in the same year, another stimulus package was announced, totaling 23.9 trillion yen. The very next year an ¥18 trillion stimulus was tried, and, in October of 2000, another stimulus for 11 trillion was announced. As economist Ben Powell points out, “Overall during the 1990s, Japan tried 10 fiscal stimulus packages totaling more than 100 trillion yen, and each failed to cure the recession,” with Japan’s nominal GDP growth rate below zero for most of the five years after 1997.

After five years in an economic wilderness, the Bank of Japan switched, during the spring of 2001, to a policy of quantitative easing — targeting the growth of the money supply instead of nominal interest rates — in order to engineer a rebound in demand growth.

The move by the Bank of Japan to quantitative easing and the large increase in liquidity that followed stopped the fall in land prices by 2003. The Bank of Japan held interest rates at zero until early 2007, when it boosted its discount rate back to 0.5 percent in two steps by mid year. But the BoJ quickly reverted back to its zero interest rate policy.

In August of 2008, the Japanese government unveiled an ¥11.5 trillion stimulus. The package, which included ¥1.8 trillion in new spending and nearly ¥10 trillion in government loans and credit guarantees, was in response to news that the Japanese economy in July suffered its biggest contraction in seven years and inflation had topped 2 percent for the first time in a decade.

Newswire reports said the new measures would include assistance to the agriculture sector, support for part-time workers to find better employment, and rebates on toll roads. Additional spending was also to flow to healthcare, housing, education, and environmental technology.

Just this past April, the Japanese government announced another ¥10 trillion stimulus program. This was after Japan’s economy shrank by a record 15.2 percent annual rate in the first quarter of 2009. This drop was on the heels of a 14.4 percent drop in the fourth quarter of 2008.

Last month, Reuters reported that the Bank of Japan reinforced its commitment to maintaining very low interest rates and may provide even further easing. “The bank said that it would not tolerate zero inflation or falling prices.” The bank left its policy rate at .1 percent and analysts see the rate staying low possibly until 2012.

According to Reuters, the Japanese government “is fretting over the risk of the economy flipping back into recession and is pushing the bank for action.” Economy flipping back into recession? Are they kidding? Japan’s GDP at the end of this year will be no higher than it was in 1992–17 lost years.

“After 17 years of bailouts and stimulus programs, the Japanese should be getting good at them,” write Bonner and Wiggin. “But it’s a little like a guy who’s getting good at suicide — if he’s so good at it, you’d think he’d be dead already.”

But Keynesians are wont to grade on a curve. Nobel laureate and New York Times columnist Paul Krugman, for one, points to Japan’s fiscal stimulus packages as having “probably prevented a weak economy from plunging into an actual depression.”

And finally, here is a video on Keynesian Economics.

Economists have either followed Friedman or Keynes for Economic Theory over the last century. Keynes is being used currently and you can judge the results for yourself. For me, it does not seem to work, nor has history shown it to have worked for any of the presidents who have based their administration on Keynesian theory anywhere in the world.

I quote one of the best authors of our generation on economics for this article.

If Milton Friedman were alive today — and there was never a time when he was more needed — he would be one hundred years old. He was born on July 31, 1912. But Professor Friedman’s death at age 94 deprived the nation of one of those rare thinkers who had both genius and common sense.

Most people would not be able to understand the complex economic analysis that won him a Nobel Prize, but people with no knowledge of economics had no trouble understanding his popular books like “Free to Choose” or the TV series of the same name.

In being able to express himself at both the highest level of his profession and also at a level that the average person could readily understand, Milton Friedman was like the economist whose theories and persona were most different from his own — John Maynard Keynes.

Like many, if not most, people who became prominent as opponents of the left, Professor Friedman began on the left. Decades later, looking back at a statement of his own from his early years, he said: “The most striking feature of this statement is how thoroughly Keynesian it is.” No one converted Milton Friedman, either in economics or in his views on social policy. His own research, analysis and experience converted him.

As a professor, he did not attempt to convert students to his political views. I made no secret of the fact that I was a Marxist when I was a student in Professor Friedman’s course, but he made no effort to change my views. He once said that anybody who was easily converted was not worth converting.

I was still a Marxist after taking Professor Friedman’s class. Working as an economist in the government converted me.

What Milton Friedman is best known for as an economist was his opposition to Keynesian economics, which had largely swept the economics profession on both sides of the Atlantic, with the notable exception of the University of Chicago, where Friedman was both trained as a student and later taught.

In the heyday of Keynesian economics, many economists believed that inflationary government policies could reduce unemployment, and early empirical data seemed to support that view. The inference was that the government could make careful trade-offs between inflation and unemployment, and thus “fine tune” the economy.

Milton Friedman challenged this view with both facts and analysis. He showed that the relationship between inflation and unemployment held only in the short run, when the inflation was unexpected. But, after everyone got used to inflation, unemployment could be just as high with high inflation as it had been with low inflation.

When both unemployment and inflation rose at the same time in the 1970s — “stagflation,” as it was called — the idea of the government “fine tuning” the economy faded away. There are still some die-hard Keynesians today who keep insisting that the government’s “stimulus” spending would have worked, if only it was bigger and lasted longer.

This is one of those heads-I-win-and-tails-you-lose arguments. Even if the government spends itself into bankruptcy and the economy still does not recover, Keynesians can always say that it would have worked if only the government had spent more.

Although Milton Friedman became someone regarded as a conservative icon, he considered himself a liberal in the original sense of the word — someone who believes in the liberty of the individual, free of government intrusions. Far from trying to conserve things as they are, he wrote a book titled “Tyranny of the Status Quo.”

Milton Friedman proposed radical changes in policies and institution ranging from the public schools to the Federal Reserve. It is liberals who want to conserve and expand the welfare state.

As a student of Professor Friedman back in 1960, I was struck by two things — his tough grading standards and the fact that he had a black secretary. This was years before affirmative action. People on the left exhibit blacks as mascots. But I never heard Milton Friedman say that he had a black secretary, though she was with him for decades. Both his grading standards and his refusal to try to be politically correct increased my respect for him.

Thomas Sowell is a senior fellow at the Hoover Institution, Stanford University, Stanford, CA 94305. His website is www.tsowell.com.

He also wrote this:

When both unemployment and inflation rose at the same time in the 1970s —”stagflation,” as it was called — the idea of the government “fine tuning” the economy faded away. There are still some die-hard Keynesians today who keep insisting that the government’s “stimulus” spending would have worked, if only it was bigger and lasted longer.

This is one of those heads-I-win-and-tails-you-lose arguments. Even if the government spends itself into bankruptcy and the economy still does not recover, Keynesians can always say that it would have worked if only the government had spent more.

Although Milton Friedman became someone regarded as a conservative icon, he considered himself a liberal in the original sense of the word — someone who believes in the liberty of the individual, free of government intrusions. Far from trying to conserve things as they are, he wrote a book titled “Tyranny of the Status Quo.”

Milton Friedman proposed radical changes in policies and institutions ranging from the public schools to the Federal Reserve. It is liberals who want to conserve and expand the welfare state.

As a student of Professor Friedman back in 1960, I was struck by two things — his tough grading standards and the fact that he had a black secretary. This was years before affirmative action. People on the left exhibit blacks as mascots. But I never heard Milton Friedman say that he had a black secretary, though she was with him for decades. Both his grading standards and his refusal to try to be politically correct increased my respect for him.